When the price of the underlying commodity in a futures contract is higher than the spot (immediate) price, the situation is known as contango. When the price of the underlying commodity for future delivery is lower, the situation is known as backwardation.

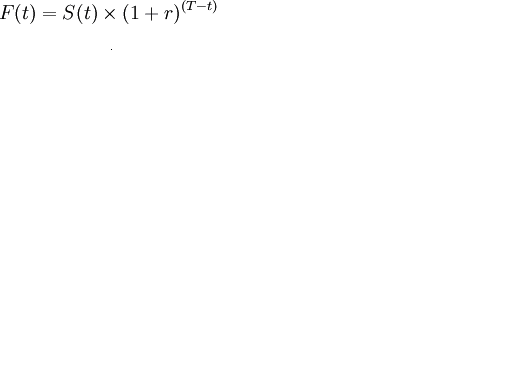

The price of a futures contract can be calculated with the following formula

where,

F(t) = future value

S(t) = present value

t = time

T = maturity

r = rate of return..

No comments:

Post a Comment